In 2020, I worked for several months as a software development contractor. This was not the first time I worked as a contractor, but this time was different. Now I knew more, especially about something called the 20% pass-through tax deduction for business entity owners (courtesy of the Tax Cuts and Jobs Act). As a human, I am an entity, and as an independent contractor, I can define myself as a business entity owner.

The other nice thing about filing as a business is that I can contribute to a pre-tax Solo 401K (a.k.a. Individual 401K – name preferred by investment companies) as both an employee and employer up to a maximum of $57,000. I can contribute $19,500 as an employee and can contribute a matching amount as an employer. Calculating the employer matching contribution, which is based upon the business income, is a little complicated so I used one of several free online calculators. (For example, assuming $40,000 income, the employer contribution is $7,434.82.)

The goal, of course, is to reduce the amount of taxes I pay. (Because I live in a state without income tax, I only need to worry about minimizing the amount of federal income tax that I pay.)

Below are the steps I took when filing federal income tax in 2020 using TurboTax Premier.

EIN for Sole Proprietorship

To keep things simple, I created a sole proprietorship business for myself just like this (imagine me snapping my fingers).

- The business name is my own full name. No need to go through the trouble to register a different name using Doing Business As (DBA), because it requires a small fee and steps like advertising in the newspaper.

- No need to incorporate as a Subchapter S Corporation (S Corp) or Limited Liability Company (LLC) because I don’t wish to pay the large yearly registration fee and don’t need the extra liability protection.

The only thing a sole proprietorship needs is an Employer Identification Number (EIN), which is used when creating a Solo 401K and filing taxes. Think of the EIN as the social security number (or more accurately, the tax identification number) for a business.

To get an EIN, do the following:

- Browse to the IRS website and click on the “Apply for an Employer ID Number (EIN)” link (located in middle of page).

- Click on the “Apply Online Now” button and follow the instructions.

- You will get an IRS notice email with your EIN.

Input Business Income

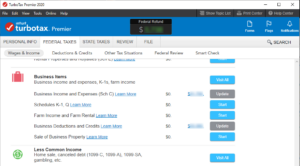

As an independent contractor, I received a Form 1099-NEC (which replaces Form 1099-MISC). In TurboTax, as an individual, I would input the 1099-NEC in “1099-MISC and Other Common Income” under Federal Taxes’ “Wages & Income”. However, as a sole proprietorship, I should input the business and 1099-NEC under “Business Items”.

Here’s how to input a business and then input the 1099-NEC under that business:

- Click on “FEDERAL TAXES” tab at the top of TurboTax.

- Click “Wages & Income” and select “I’ll choose what I work on”.

Locate “Business Income and Expenses (Sch C)” under “Business Items” and click Start.

Locate “Business Income and Expenses (Sch C)” under “Business Items” and click Start.

- Click on “Add A Business”.

- Input a description of the business (ex: “Contracting – Software Development”). Click Continue (I will omit this instruction from this point onwards).

- Check “I use my name as the name of my business”.

- Input the address. I used my home address.

- Select Yes and input the EIN.

- Lookup the “Business Code”. I ended up with 541510 which is “Computer systems design & related services”.

- I picked “Cash Method” because it is the simplest method – income and expenses are recorded in the tax year that they occur in.

- Check “Yes, I played an active role in business operations”.

- Check “Enter my business info myself”.

- Check “No” for “Did you make any payments that required you to issue a form 1099?”. (I’m assuming you are not subcontracting.)

- Leave everything unchecked for “uncommon situations” unless they apply to you.

- Click on “Add a Form 1099-NEC” to input your income under the business and fill in the requested information.

- For the following screens, I left them blank (or with default values) because they didn’t apply to me as a software developer. I don’t deal with goods and don’t travel.

- For Business Expenses, I left “Home office expenses” blank because it seemed too troublesome to calculate the space (part of my bedroom) that I used. Also, if I calculated it wrong, it might raise an audit flag. (I guess if you have a large home office room, it might be worth it to take the expense.)

- Muy Importante! Select “Yes, XXXX is a qualified business income” when asked “Is this Qualified Business Income (QBI)?”. Answering positively will give you the 20% business income tax deduction.

- At the end, if you did it right, the last screen should say “Great news! You get a tax break”. And then you will see the pitiful amount of deduction you get. No, you don’t get 20% of your income deducted. On a $50,000 business income, you are lucky to get a $1000 deduction. (Like anything IRS related, the QBI deduction calculations are a bit complex… google it.)

Clawing money back from the government is hard work. Every little bit counts, folks!

Input Pre-Tax Solo 401K Contribution as Business Deduction

TurboTax handles the pre-tax Solo 401K contribution as a business deduction. I guess it makes sense because the pre-tax Solo 401K reduces the business income.

Here’s how to input the Solo 401K contribution:

- Locate “Business Deductions and Credits” under “Business Items” and click Start.

- Locate “Self-employed retirement plans” and click Start.

- Answer Yes to “Did you contribute to an Individual or Roth 401(k) plan?”

- Input $19,500 into the “Elective Deferrals” box. ($19,500 is the limit for employee contribution to Solo 401K in 2020.)

- Check the checkbox called “Maximize Contribution to Individual 401(k)” so it will calculate maximum number for the “Employer Matching (Profit Sharing) Contributions” field.

- A couple of screens later, a summary will tell you the calculated maximum employer matching contribution to fund. (This should match the number provided by the online Solo 401K calculators.)

- If you don’t plan to contribute the maximum employer matching contribution, you can leave the checkbox unchecked and manually input a number into the “Employer Matching (Profit Sharing) Contributions” field.

Don’t forget to open up a Solo 401K at your favorite investment company and contribute both employee and employer portions to it. (You can open an Individual 401K online at Vanguard; though their employer website interface is clunky and old-fashioned.)

Note: You can contribute to your Solo 401K up until the personal tax-filing deadline (April 15).

Input Health Insurance Payments as Business Deduction

Another nice benefit of filing as a sole proprietorship is that the health insurance payments are considered a business deduction. As a business, I am paying health insurance expenses for my one and only employee (me).

TurboTax has a subsection called “Self-employed health insurance paid”, under “Business Deductions and Credits”, but this does not apply for insurance purchased from the Health Insurance Marketplace (a.k.a. Exchange). I think it only applies to health insurance plans purchased directly from the health insurance companies.

Instead, we need to input the Exchange-related Form 1095-A by doing the following:

- Click on “Deductions & Credits” sub-tab and select “I’ll choose what I work on”.

- Locate “Affordable Care Act (Form 1095-A)” under “Medical” section and click Start.

- Click the “Add” button and input the information from the Form 1095-A.

- Check “I’m self-employed and bought a Marketplace plan”. This will treat the medical insurance payments as a business deduction.

- The description for the business (there should only be one) should be selected already. Select January and December as the first and last months the business operated to deduct all the insurance payments. (Technically, my sole proprietorship existed even in the months I did not do any work as a contractor.)

Input Pre-Tax HSA Contribution as Deduction

For 2020, I selected a Health Savings Account (HSA) qualified plan from the Health Insurance Exchange. It cost a bit more, but it allowed me to make a pre-tax contribution of $3550. (The HSA contribution is considered a deduction because it reduces non-business income.)

Note: When searching health plans in the exchange, look for a filter called “HSA Qualified” to only show plans that allow HSA contributions.

Here’s how to input the pre-tax HSA Contribution:

- Under “Deductions & Credits” and “Medical”, look for “1099-SA, HSA, MSA” and click Start.

- Select “Health Savings Account (HSA)”.

- I answer No to both “use your HSA” and “inherit this HSA” because they don’t apply.

- Input the HSA contribution amount into the “Any contributions you personally made (not through your employer)” field.

- I answer No to both “employers make contributions” and “have Medicare”.

- Select “Yes, I was covered by an HDHP during at least one month during 2020”. (HDHP stands for High Deductible Health Plan, which describes every plan in the Health Exchange.) And select “I was covered by a Self only plan every month of the year”.

- Answer No to “overfund your HSA” in the previous year.

Input After-Tax Roth IRA Contribution

If your income, or more accurately your Modified Adjusted Gross Income (MAGI), is less than the Roth IRA income limit ($139,000 in 2020), I recommend contributing the maximum $6000 to a Roth IRA account. In case you ask, yes, you are allowed to contribute to both a Solo 401K and Roth IRA at the same time.

Note: The Roth IRA contribution is after-tax so it doesn’t affect your current year’s income tax. The IRS just wants to know about it.

Why invest in an after-tax Roth IRA? The most important reason is that when you withdraw after retirement age, the gains are not taxable. (FYI, you can withdraw the principal without penalty after 5 years, but why would you want to do that?)

Here’s how to input the Roth IRA Contribution:

- Under “Deductions & Credits” and “Retirement and Investments”, look for “Traditional and Roth IRA Contributions” and click Start.

- Check the box for “Roth IRA”.

- Answer No to “Is This a Repayment of a Retirement Distribution?”. (I hope you don’t answer Yes.)

- Input the amount into the “Your Roth Contribution” field.

- Answer No to “Switch from a Roth To a Traditional IRA?” (Gosh, why would you ever want to do such a thing!)

- I hope you can answer No to the remaining two screens.

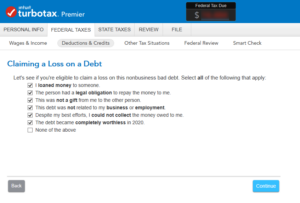

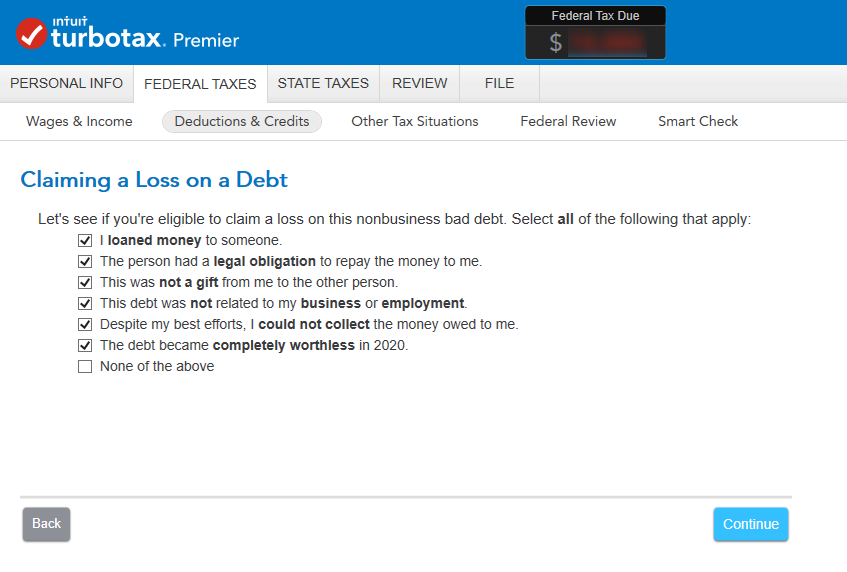

Input Non-business Bad Debt as Deduction

If you have made a personal loan and don’t expect to ever get paid back, you can claim it as a non-business deduction.

Quicken states “A nonbusiness bad debt is deductible as a short-term capital loss no matter how long the debt was owed to you. Capital losses are limited to $3000 more than capital gains per year.”

Here’s how to input a non-business bad debt:

- Under “Deductions & Credits” and “Other Deductions and Credits”, look for “Nonbusiness Bad Debt” and click Start.

- Answer Yes to “Did a personal debt somebody owed you become uncollectible in 2020?”

Select all options except “None of the above” for “Claiming a Loss on a Debt”. All options need to apply in order for this to be considered a non-business bad debt.

Select all options except “None of the above” for “Claiming a Loss on a Debt”. All options need to apply in order for this to be considered a non-business bad debt.

- Input all the requested information under “Your Loan Qualifies” as best you can. Reasons I’ve decided that a debt was worthless include “he declared bankruptcy” and “he is a compulsive gambler so all hope is lost”.

TurboTax editions for 2019 and earlier years placed the non-business bad debt in an obscure location (under “Wages & Incomes”, “Investment Income”, “Stocks, Mutual Funds, Bonds, Other”, and “Uncollectible Debt (Nonbusiness Bad Debt)” as type of investment).

If you need to revise 2019 or earlier years, use the search function:

- Click on the magnifying glass icon with text SEARCH in the top-right corner.

- Input “nonbusiness bad debt” and hit return.

- Click on the “Jump to nonbusiness bad debt” link (first result).

Note: The nice thing about TurboTax is that it will track the carryover (in case the capital losses exceed $3000) and automatically apply it to next year’s income tax return. To take advantage of this function, you must use TurboTax every year though.

Input Foreign Tax Credit

If you have an investment in a foreign company and receive dividends, you will need to pay foreign tax. The IRS allows you to treat the foreign tax as a deduction or a credit. I recommend taking a credit because it would usually reduce your tax more than a deduction would, especially if you take the standard deduction (which renders the foreign tax deduction ineffective).

Before inputting the foreign tax credit, make sure you have reported all your Form 1099-DIVs to TurboTax.

Here’s how to input the foreign tax credit:

- Under “Deductions & Credits” and “Estimates and Other Taxes Paid”, look for “Foreign Taxes” and click Start.

- Answer “Take a Credit” for “Do You Want the Deduction or the Credit?”.

- Select the countries that have charged you a foreign tax under “Where Did You Receive Dividend Income From?”

- Input “Various” if you have a mutual fund that invests in more than one foreign country, such as Vanguard’s International Index Fund.

Note: The foreign tax limit is $337 for 2020, which means that you might need to carry forward the excess (for up to 10 years).

Deduct Cash Donations Up To $300 (Without Itemizing)

In 2020, even though you take the standard deduction, you can still deduct up to $300 in cash donations made to charity. This is an amazing change because previously, if you took the standard deduction (and did not itemize), you could not deduct anything else.

So when determining whether to itemize deductions or not, compare the itemized total against the standard deduction plus $300.

Note: The previous year’s state income tax is deductible in this year’s federal income tax return. (Likewise, the previous year’s state income tax refund will increase this year’s federal income tax due amount.) In high income tax states like California or New York, the state income tax will usually make the itemized total greater than the standard deduction.

Here’s how to input your cash donations:

- Under “Deductions & Credits” and “Charitable Donations”, look for “Donations to Charity in 2020” and click Start.

- Answer Yes to “Do you want to enter your donations for 2020?”.

- Enter the name of the charity and click the Add button next to “Money” to add your cash donation.

Update: I just inputted cash donations into my 2021 return and noticed that it did not affect my refund amount. TurboTax may not have implemented this correctly. Unfortunately, I had not checked whether cash donations had made a difference in my 2020 return.

Input Car Registration Fee as Deduction

If you are not taking the standard deduction (usually because your total deductions exceed the standard deduction), then I suggest inputting the tax portion of your vehicle registration fee as a non-business deduction. (On your DMV vehicle registration receipt, look for something like “GOV SERVICES TAX”. That is the part that can be deducted.)

Here’s how to input the car registration fee:

- Under “Deductions & Credits” and “Cars and Other Things You Own”, look for “Car Registration Fees” and click Start.

- Fill in the “Vehicle Make & Model” and enter the tax portion under “Amount”.

The tax portion of the car registration fee may be small, but when minimizing the income tax you pay, again, every little bit counts.

I hope that the above will help you to minimize your income tax.